Balancing debt repayment with consistent saving feels like walking a tightrope. One misstep — an unexpected car repair or a forgotten bill — can send your entire budget crashing. Yet the most financially resilient households don't choose between paying off debt and saving. They automate both.

Automation removes emotion from money decisions. When your savings account and debt payments run on autopilot, you stop negotiating with yourself every payday. This frees up mental energy while building credit-ready momentum — the kind that improves your credit utilisation, demonstrates payment history, and prepares you for major life events like buying a home or starting a business.

Table of Contents

Why Automation Creates Credit-ready Momentum

Automation works because it bypasses willpower. When you schedule transfers the day after payday, you never see that money in your checking account. You can't spend what isn't there. This "pay yourself first" approach builds savings while ensuring debt payments arrive on time — the single most important factor in your credit score.

Credit-ready momentum means your financial habits actively prepare you for future borrowing needs. Lenders want to see:

- On-time payments over a sustained period

- Low credit utilisation (below 30%)

- A mix of credit types managed responsibly

- Adequate savings reserves for emergencies

Automated systems check every box. Consistent payments build history. Growing savings reduce your reliance on credit cards during emergencies, keeping utilisation low. The result: when you need a mortgage or auto loan, your profile signals low risk.

The Debt Payoff + Savings Dual-track Strategy

Most people believe they must choose between debt freedom and building savings. The "avalanche" method says pay highest-interest debt first. The "snowflake" method says attack smallest balances. Neither typically prioritises saving simultaneously.

A dual-track strategy changes the game. By automating a modest savings contribution — even $25 per week — alongside your minimum debt payments, you create a safety net that prevents new debt when life happens. This is where tools like a Wooden Money Saving Box or a structured envelope system keep you accountable.

The 50/30/20 Automation Framework

- 50% to needs (automated bill pay including minimum debt payments)

- 30% to wants (discretionary, manually managed)

- 20% to financial goals (split between debt snowball/avalanche and savings)

Set up recurring transfers. Payday hits → savings transfer fires first → debt payment fires second → remaining cash covers needs and wants.

Pairing Automation with a Physical Savings Challenge

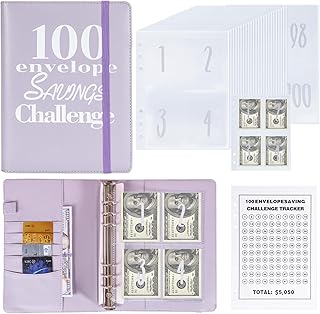

Digital automation handles the logistics, but a physical savings tool builds momentum you can see and touch. The 100 Envelopes Money Saving Challenge (Price: $8.99, Rating: 4.7) provides a proven structure for goal-oriented saving.

Each envelope represents a dollar amount from $1 to $100. Draw one envelope daily or weekly and deposit that amount into your savings account. Over 100 draws, you accumulate $5,050 — enough for a solid emergency fund or a significant debt payment.

Why this works with automation: Set up a recurring transfer of $50.50 per week ($5,050 ÷ 100 weeks) to your savings account. Use the envelope binder as a visual tracker. When you see envelopes filling up, your brain registers progress. This combination of digital automation and physical tracking accelerates credit-ready momentum.

Product Spotlight: Budgeting Binders

For those who prefer an all-in-one system, the SKYDUE Budget Binder (Price: $8.98, Rating: 4.7) combines cash envelopes with expense tracking sheets. It pairs perfectly with automated transfers — your digital savings feed your physical binder.

Wooden Savings Boxes for Tangible Goal Tracking

Wooden savings boxes offer a satisfyingly tactile way to track progress toward specific targets. The 10000 Kakeibo Wooden Money Saving Challenge Box (Price: $7.99, Rating: 4.4) uses the Japanese kakeibo method — a mindful savings approach that emphasises intentional spending.

How to automate with a wooden box:

- Set a weekly automated transfer of $50 to your checking account

- Withdraw that cash and place it in the wooden box

- Log each deposit on the built-in progress tracker

- When the box is full, make a lump-sum debt payment or move funds to a high-yield savings account

The Wooden Money Saving Box for $10,000 Target (Price: $7.99, Rating: 4.5) offers twelve different savings targets (from $500 to $10,000), making it adaptable whether you're saving for a vacation, a wedding, or a debt snowball fund.

Envelope Challenge Systems for Accountability

The envelope method remains one of the most effective budgeting systems because it imposes a hard spending limit. When the cash is gone, spending stops. The NICOOTH 100 Envelopes Money Saving Binder (Price: $6.48, Rating: 4.7) takes this classic approach and organises it into a portable A5 binder.

Automation + envelope method hybrid:

- Automate transfers to a dedicated savings account each payday

- Withdraw a weekly cash allowance for variable expenses (groceries, dining, entertainment)

- Use the envelope binder to allocate that cash into categories

- Any unspent cash at week's end goes into a "debt payoff" envelope

This system prevents overspending while building a cash buffer that protects your credit. When you have cash set aside, you don't need to reach for a credit card when unexpected expenses arise.

The Sooez 100 Envelopes Money Saving Challenge (Price: $7.99, Rating: 4.7) includes pre-numbered envelopes and a challenge tracker, simplifying the process of reaching $5,050.

Using Automation to Prepare for Life Events

Life events — both expected and unexpected — test your financial stability. Automation ensures you're prepared without last-minute scrambling.

| Life Event | Automated Savings Strategy | Target Amount | Timeline |

|---|---|---|---|

| Wedding | Weekly transfer to dedicated account | $5,000–$30,000 | 12–24 months |

| New baby | Bi-weekly transfer to 529 or savings | $3,000–$10,000 | 9 months |

| Home purchase | Monthly transfer to high-yield account | 3–6% of purchase price | 12–36 months |

| Emergency fund | Automatic transfer each payday | 3–6 months of expenses | 6–18 months |

| Car replacement | Weekly transfer to sinking fund | $5,000–$15,000 | 36–60 months |

Each of these goals benefits from a visual tracking tool. The KYODOLED Cash Box with Key Lock (Price: $22.99, Rating: 4.7) provides secure storage for cash savings while you build toward these targets. Use it to hold physical deposits that complement your digital automated transfers.

The Credit Score Impact of Automated Savings

Automated savings affects your credit score through three channels:

1. Payment history (35% of FICO score): When savings cover unexpected expenses, you never miss a debt payment. Set up automated minimum payments from your savings account to ensure zero late payments.

2. Credit utilisation (30% of FICO score): A growing savings account means you can pay credit card balances in full each month. Keep utilisation below 10% for maximum score impact.

3. Credit mix (10% of FICO score): As your savings accumulate, you become a lower-risk borrower. Lenders are more willing to extend installment loans (auto, mortgage) when they see consistent savings behaviour.

The 2PCS 100 Envelopes Money Saving Challenge (Price: $17.09, Rating: 4.7) includes two binders — one for savings goals and one for debt payments. This dual-binder approach mirrors the dual-track strategy: automate both, track both visually, and watch your credit profile strengthen.

Building Your Personal Automation System

Creating a credit-ready automation system requires four steps:

- Audit your current cash flow. Know exactly when money arrives and when bills are due.

- Set up a high-yield savings account. Keep it separate from your checking account to reduce temptation.

- Schedule transfers on payday. Savings first, debt second, then spending.

- Choose a visual tracking tool. A wooden savings box or envelope binder keeps you motivated.

The 10000 Savings Challenge Box, Wooden Money Saving Piggy Bank (Price: $6.99, Rating: 4.2) targets a $10,000 goal — an ambitious but achievable target for credit-ready momentum.

Why This Approach Beats "Debt First, Save Later"

The conventional wisdom says pay all debt before saving. This approach fails because:

- Emergencies happen and force new debt

- You miss the compounding growth of early savings

- You develop no savings habit for future goals

- Your credit score remains volatile

Automating both tracks simultaneously creates sustainable momentum. Your debt decreases while your savings increase. Your credit score stabilises and improves. When a life event arrives — a wedding, a baby, a home purchase — you're ready.

FAQ: Debt Payoff Plus Savings Automation

Q: Should I automate savings before paying off high-interest debt?

A: Yes, but keep the savings modest — $500 to $1,000 as a starter emergency fund. Then prioritise high-interest debt. Once debt is under control, increase the automated savings rate.

Q: How much should I automate toward savings while in debt?

A: Start with 5–10% of your net income. If that feels tight, begin with $25 per week. The habit matters more than the amount. Increase as your debt decreases.

Q: Can automation really improve my credit score?

A: Absolutely. Automated payments ensure on-time history. Automated savings keep credit utilisation low. Both factors account for 65% of your FICO score.

Q: What is the best physical tool to pair with automated savings?

A: The best tool is one you'll use consistently. Wooden savings boxes work well for goal-based savers. Envelope binders suit those who prefer category-based tracking. Choose based on your personality and goals.

Q: How do I handle irregular income with automation?

A: Automate a percentage transfer rather than a fixed amount. When income fluctuates, a percentage-based automation keeps you saving without overdrawing.

Q: Should I use a physical cash system if I already automate digitally?

A: Yes. Physical systems provide visual reinforcement that digital accounts cannot match. They transform abstract numbers into tangible progress, which sustains motivation over months and years.