Most people view budgeting as a financial straitjacket. They focus on what they can't spend or track every penny without a clear destination.

Goal-based budgeting flips the script entirely. It starts with your dreams—a debt-free life, a $10,000 emergency fund, or a family vacation—and works backward to your monthly cash flow. You stop managing pennies and start fueling your future.

Instead of asking, "Where did my money go?" you ask, "What did my money just accomplish?" This shift turns a chore into an exciting path toward specific outcomes.

Table of Contents

Why Traditional Budgeting Fails (And Goal-Based Budgeting Succeeds)

Traditional budgets rely on willpower. They tell you what you cannot do. Goal-based budgets rely on a compelling why. When your savings account is tied to the specific outcome of "buying a house in 3 years," skipping the daily latte feels like progress, not deprivation.

| Feature | Traditional Budgeting | Goal-Based Budgeting |

|---|---|---|

| Focus | Restriction & Tracking | Action & Achievement |

| Motivation | External (Rules) | Internal (Dreams) |

| Cash Flow View | "Leftover Money" | "Outcome Fuel" |

| Beginner Friendly | No (Feels punitive) | Yes (Feels exciting) |

| Success Metric | Staying under budget | Reaching milestones |

The data backs this up. People who use visual saving money tools—like the Wooden Money Saving Box, Cash Vault Savings Box for $10000—are significantly more likely to hit their targets because they see progress daily.

The 4-Step Framework to Turn Cash Flow into Outcomes

Applying goal-based budgeting is simple. You don't need a finance degree. You need clarity and the right systems.

Step 1: Define Your "Specific Outcomes" (SMART Goals)

Vague goals create vague budgets. Specific outcomes create momentum.

- Debt Payoff: "Pay off $5,000 credit card debt in 10 months using $500 monthly cash flow."

- Savings Milestone: "Save $10,000 for a down payment by December 2025."

- Travel Fund: "Accumulate $1,200 for a vacation in 6 months."

Write these down. Every dollar in your budget should have a name and a purpose.

Step 2: Calculate Your "Free Cash Flow"

This is your financial weapon. Free cash flow = Total monthly income – Fixed essential expenses (rent, utilities, minimum debt payments, groceries).

Example:

- Income: $4,000

- Fixed Expenses: $3,200

- Free Cash Flow: $800

This $800 is not "extra." It is the fuel for your specific outcomes.

Step 3: Create "Goal Buckets"

You must separate your money mentally and physically. Goal buckets prevent you from spending your vacation fund on takeout.

For absolute beginners, physical systems work best. The 100 Envelopes Money Saving Challenge, 100 Envelope Challenge Binder ($8.99, 4.7 rating) forces you to allocate cash to a numbered envelope system. Each envelope is a mini-milestone.

This binder is designed to save $5,050—a very specific outcome. You match the envelope number to the dollar amount. It gamifies the process.

Step 4: Automate & Track

Set up automatic transfers on payday. If you use physical tools, schedule a weekly "cash stuffing" session.

The NICOOTH 100 Envelopes Money Saving Binder A5 ($6.48, 4.7 rating) is an ultra-budget-friendly way to start. It includes the binder, envelopes, and tracking sheets so you can monitor your monthly cash flow against your target.

Best Tools to Visualize Your Goal-Based Budget

You need tactile feedback to stay motivated. Here are the top-rated tools that align perfectly with goal-based budgeting.

The $10,000 Savings Challenge Box

The Wooden Money Saving Box, Piggy Bank for Kids & Adults ($7.99, 4.5 rating) is a reusable cash vault. It features a progress tracker and marker.

- Best for: Large, long-term goals (House, Car, Emergency Fund).

- Why it works: You physically "smash" it when done.

The Budget Binder System

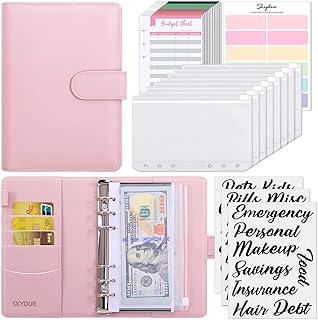

For managing multiple outcomes (debt + savings), the SKYDUE Budget Binder, Money Saving Binder with Zipper Envelopes ($8.98, 4.7 rating) is excellent.

- Best for: Cash stuffing enthusiasts.

- Why it works: Zippered envelopes keep different goals separate.

The 2-Pack Challenge

If you are budgeting with a partner, the 2PCS 100 Envelopes Money Saving Challenge ($17.09, 4.7 rating) gives you pink and black binders. You both work toward specific savings milestones.

Example: Applying Goal-Based Budgeting to Debt vs. Savings

Let's use a real scenario. You have $500 free cash flow per month.

Scenario A: Aggressive Debt Payoff

- Outcome: Financial Freedom.

- Action: Allocate $400 to debt snowball. Allocate $100 to emergency starter fund.

- Tool: Use the KYODOLED Cash Box with Key Lock ($22.99) to store the emergency cash. Keeping it separate ensures you don't spend it.

Scenario B: Saving for a Milestone

- Outcome: $10,000 Vacation Fund in 12 months.

- Action: Allocate $500 monthly. That's $6,000 + interest.

- Tool: The 10000 Kakeibo Wooden Money Saving Challenge Box ($7.99, 4.4 rating) is perfect. It has 10 amounts to track. Once you fill it, you smash it open to achieve your outcome.

The Psychology of "Specific Outcomes"

Goal-based budgeting works because it triggers dopamine—the reward chemical.

Every time you check off a box on the Sooez 100 Envelopes Money Saving Challenge ($7.99, 4.7 rating), you get a small hit of accomplishment.

Why physical tools beat apps for beginners:

- Tactile feedback: You see the stack grow.

- Commitment device: Smashing the 10000 Savings Challenge Box ($6.99, 4.2 rating) requires physical effort.

- Clarity: You know exactly how much you have for each specific outcome.

FAQ: Goal-based Budgeting for Beginners

What is goal-based budgeting?

Goal-based budgeting is a method where you allocate your income to specific financial goals (e.g., debt payoff, vacation savings) before assigning money to discretionary spending. It ties your monthly cash flow directly to desired outcomes.

How do I start goal-based budgeting with a monthly cash flow?

First, define your specific outcomes. Second, calculate your free cash flow (Income – Fixed Bills). Third, create buckets for each goal. Fourth, automate transfers or use physical tools like a money saving challenge box to track progress.

What is the 100 envelope challenge?

The 100 envelope challenge involves numbering 100 envelopes from 1 to 100 and saving the corresponding dollar amount each day or week. By the end, you save $5,050 towards a specific goal. Products like the Sooez 100 Envelopes Money Saving Challenge binder help organize this process.

Should I pay off debt or save money first?

Generally, it's recommended to save a small emergency fund ($1,000) first, then aggressively pay off high-interest debt, and finally save for larger milestones. Goal-based budgeting allows you to allocate cash flow to both simultaneously if your income allows.

Is goal-based budgeting effective for irregular income?

Yes. It forces you to prioritize. When you receive income, you fill your "outcome buckets" first. This ensures your goals are funded, even if discretionary spending fluctuates.

Start today. Pick one specific outcome. Calculate your free cash flow. Grab a Wooden Money Saving Box or a 100 Envelope Binder and watch your money transform from random expenses into intentional achievements.